How AI-Powered Lending Could Transform Credit Access for India's MSMEs.

How AI-Powered Lending Could Transform Credit Access for India's MSMEs.

Why A lot of MSMEs Still Struggle to Get Loans

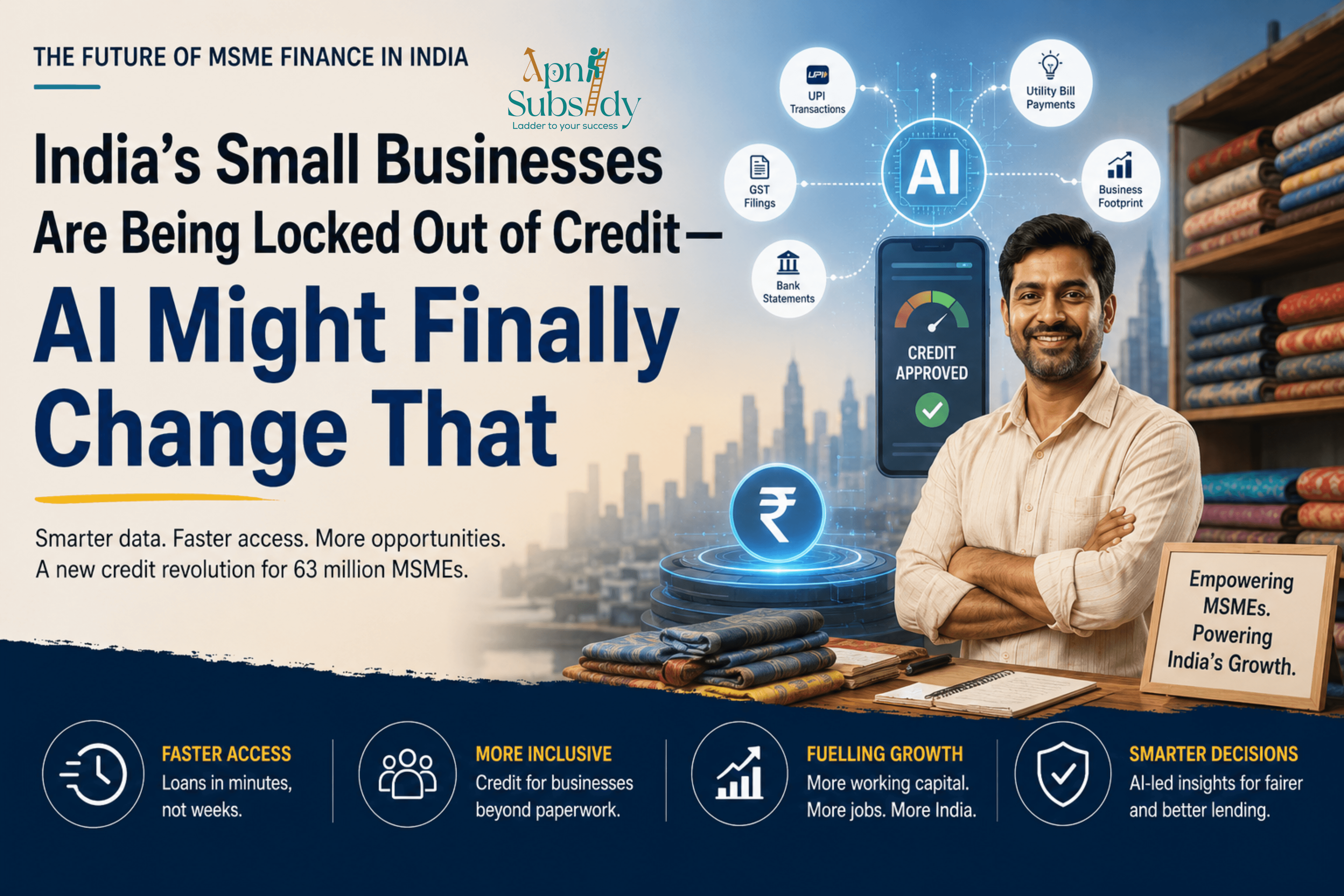

For decades, one of the biggest challenges faced by India's Micro, Small, and Medium Enterprises (MSMEs) has been access to formal credit. Despite contributing significantly to the country's economy, many small businesses continue to be rejected by banks for one simple reason—they don't appear creditworthy on paper.

A small footwear manufacturer in Agra or a garment exporter in Surat may process thousands of UPI payments every month, file GST returns regularly, and generate consistent revenue. Yet, without a strong credit history or collateral, securing a business loan remains extremely difficult.

This gap between business performance and loan eligibility has left lots of MSMEs dependent on informal lenders charging high interest rates.

AI Could Be the Solution to India's Credit Gap

According to a Press Information Bureau (PIB) release issued in May 2026, AI-powered lending models could help bridge India's estimated $130–170 billion MSME credit gap.

Instead of relying only on traditional credit scores like CIBIL, AI-based systems evaluate alternative financial indicators such as:

GST return history

UPI transaction records

Bank statements

Utility bill payments

Digital cash flow patterns

These data points provide lenders with a much broader picture of how a business actually operates, making it easier to identify financially responsible borrowers who may otherwise be overlooked.

Moving Beyond Traditional Credit Scores

Conventional lending models often fail to capture the reality of small businesses in India. Many entrepreneurs mix personal and business finances or operate without extensive formal documentation.

AI changes this approach by analyzing actual financial behaviour instead of only past borrowing history.

For example, a business that consistently pays electricity bills on time, files GST returns regularly, and receives stable digital payments demonstrates reliability—even if it has never taken a formal loan before.

This shift has the potential to make lending far more inclusive.

The Role of the Unified Lending Interface (ULI)

Supporting this transformation is the Unified Lending Interface (ULI), developed by the Reserve Bank of India as part of India's growing digital public infrastructure.

Launched in pilot mode in August 2023, ULI aims to simplify and accelerate the lending process by connecting lenders with verified financial data through a standardized platform.

By December 2025:

64 lenders (41 banks and 23 NBFCs) had joined the platform.

More than 136 data services were being used across 12 different loan journeys.

Much like UPI revolutionized digital payments, ULI aims to modernize how credit is delivered across the country.

The Massive Credit Challenge Facing MSMEs

India has approximately 63–64 million MSMEs, yet only around 14% have access to formal credit.

Nearly half of the sector's total credit demand remains unmet.

As a result, many businesses rely on:

Local moneylenders

Informal borrowing networks

Family financing

Rotating credit societies

These options often come with significantly higher interest rates, reducing profitability and limiting business growth.

How the Account Aggregator Framework Fits In

Alongside ULI, the Account Aggregator (AA) framework plays an important role in enabling digital lending.

The consent-based system allows businesses to securely share financial information—including bank accounts, GST records, and transaction history—with lenders.

More than 2.6 billion accounts have been enabled for data sharing, while over 252.9 million users have linked their accounts to the framework.

In practice, this means loan applicants can submit verified financial information within minutes instead of collecting paperwork from multiple sources.

In pilot projects, ULI has already reduced Kisan Credit Card loan processing times from four to six weeks to nearly ten minutes.

Whether MSME lending can achieve similar efficiency at scale remains to be seen.

Technology Alone Cannot Eliminate Risk

While AI can improve credit assessment, it cannot remove lending risks entirely.

Banks remain cautious because many small businesses experience:

Volatile cash flows

Limited documentation

Higher business failure rates

Even advanced AI models can be manipulated if borrowers understand the variables being evaluated.

Expanding loan eligibility also does not automatically reduce borrowing costs or guarantee approvals.

Human judgment and risk management will continue to play an important role.

Data Privacy Deserves Equal Attention

Another important concern is data privacy.

Although the Account Aggregator framework operates on user consent, many small business owners may not fully understand what information they are sharing or how it will be used.

A business owner seeking urgent financing might simply tap "Allow" without appreciating the long-term implications of granting access to sensitive financial data.

As digital lending expands, ensuring informed consent and strong data protection will be just as important as improving access to credit.

A Promising Direction for India's Economy

Despite these challenges, the broader direction is encouraging.

MSMEs contribute nearly 30% of India's GDP and generate employment for millions of people. Providing affordable and timely access to working capital could significantly boost business expansion, exports, innovation, and job creation.

By leveraging existing digital infrastructure—including Aadhaar, UPI, GST systems, ULI, and the Account Aggregator framework—India is attempting to transform not just payments but the entire lending ecosystem.

Conclusion

AI-driven lending has the potential to fundamentally reshape how India's MSMEs access finance. By evaluating real business activity instead of relying solely on traditional credit scores, lenders can make more informed decisions and extend credit to deserving businesses that were previously excluded.

However, successful implementation will depend on responsible data usage, strong privacy safeguards, and widespread adoption by financial institutions. If these challenges are addressed effectively, AI-powered lending could become a game changer for millions of small businesses and a major catalyst for India's long-term economic growth.

Tags

Work With Us

Need help identifying the right subsidy, preparing documentation, or maximizing claim value? Our team can guide you end to end.

Get in Touch