India's Digital Payments Just Set a Record No One Predicted Ten Years Ago

India's Digital Payments Just Set a Record No One Predicted Ten Years Ago

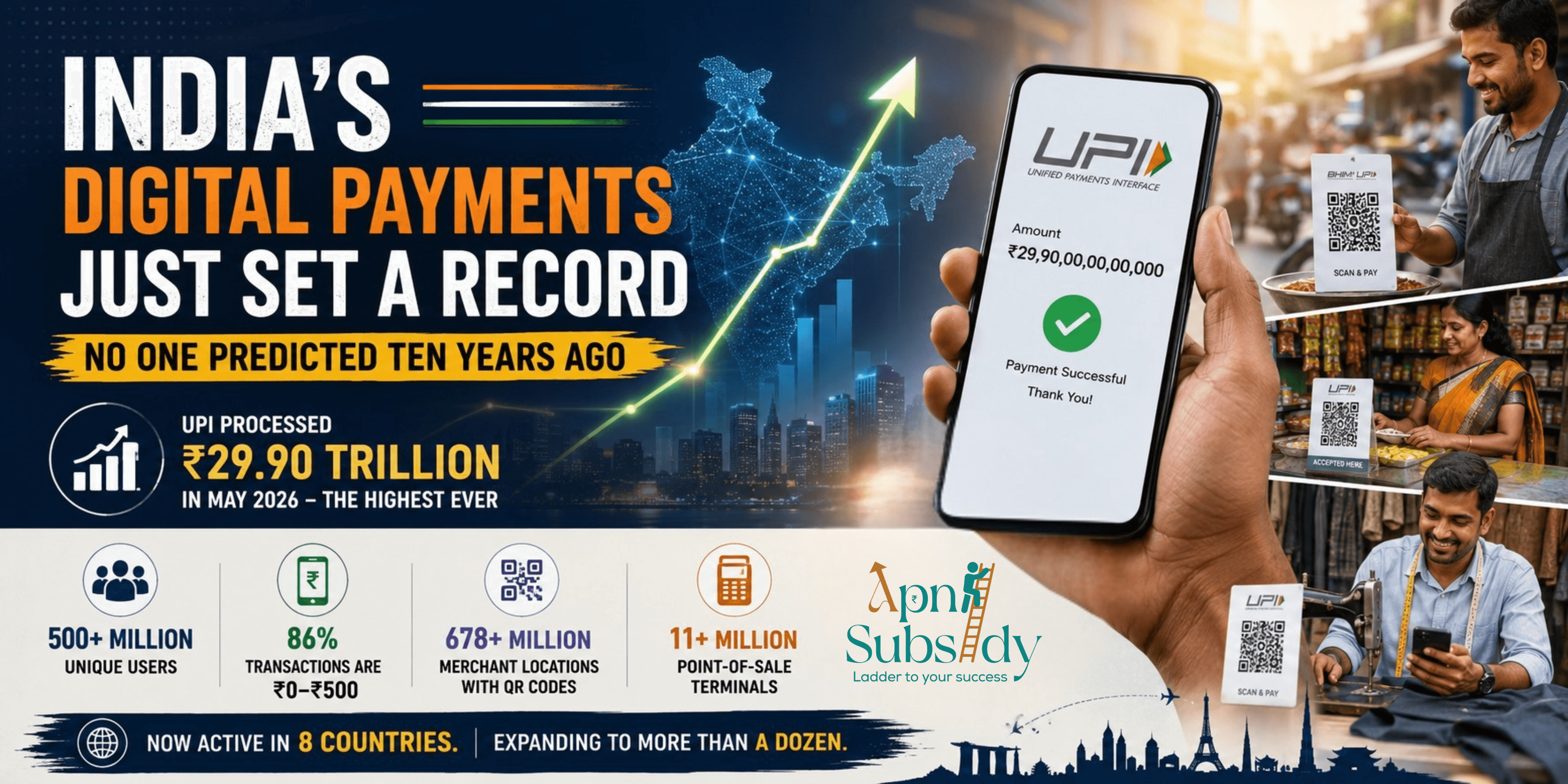

In May 2026, India achieved a milestone that would have seemed almost unimaginable a decade ago. The country's Unified Payments Interface (UPI) processed nearly ₹29.90 trillion (₹29.90 lakh crore) in transactions in a single month-the highest monthly transaction value since the platform launched in 2016.

The volume was just as remarkable. Indians completed 23.2 billion transactions through UPI during May, another all-time record and a 4 percent increase over the previous month.

To understand the scale, consider this: India's entire GDP in 2015 was roughly ₹135 lakh crore. Today, UPI alone processes nearly a quarter of that amount every month through a digital payments system that did not even exist ten years ago.

More Than Just Big Numbers

What makes this achievement significant is not merely the size of the transactions but what they reveal about how Indians now handle money.

A street-food vendor in Nagpur accepts payments through a QR code. A kirana store owner in Patna manages daily collections through a smartphone. A tailor in Coimbatore receives advance payments from customers hundreds of kilometers away.

These are no longer unusual examples. They have become part of everyday life across India.

Built on Millions of Small Purchases

UPI's success has been driven by its extraordinary reach. By early 2026, the platform had crossed 500 million unique users.

Interestingly, the vast majority of transactions are not large purchases. Around 86 percent of UPI transactions fall between ₹0 and ₹500, showing that the platform has become deeply embedded in daily spending habits-from buying tea and vegetables to paying for transport and meals.

The record-breaking numbers are not the result of a few large transactions. They are built on millions of small payments made every day by ordinary Indians.

A Massive Merchant Network

The merchant ecosystem has expanded alongside user adoption.

Today, QR codes can be found at more than 678 million merchant locations across the country, while the number of point-of-sale terminals has crossed 11 million.

Yet the story is not complete. Nearly 70 percent of India's postal codes still have fewer than 500 active UPI merchants, suggesting that large parts of the country remain underpenetrated and continue to rely heavily on cash.

The growth has been remarkable, but the opportunity for expansion remains enormous.

Why Small Businesses Benefit the Most

For small business owners, UPI has solved several long-standing challenges.

Before digital payments became widespread, merchants often had to choose between:

Cash, which was difficult to track and vulnerable to loss.

Cheques, which required days for settlement.

Card machines, which involved additional costs and infrastructure.

UPI simplified the process by making payments instant, inexpensive, and easy to record. A smartphone and a printed QR code are often all a business needs to start accepting digital payments.

The resulting digital transaction history also helps with bookkeeping, financial planning, and access to formal credit.

Growth That Shows No Sign of Slowing

UPI's expansion has continued steadily year after year.

In December 2025, the platform processed 21.63 billion transactions. Just five months later, that figure had climbed to 23.2 billion transactions.

According to government data, UPI transaction values during the first nine months of FY26 had already exceeded ₹230 lakh crore, surpassing the total value processed during the entire FY23 financial year.

The trend suggests that digital payments are still growing rapidly rather than approaching saturation.

India's Payment System Goes Global

UPI is no longer just an Indian success story.

The platform is now operational in eight countries, including Singapore, the UAE, France, Nepal, and Bhutan.

This means an Indian tourist in Paris can pay at participating merchants using the same app they use at home. It also enables Indian workers abroad to transfer money more efficiently and at lower cost than many traditional remittance channels.

The National Payments Corporation of India (NPCI) has stated its intention to expand UPI to more than a dozen countries, particularly in East Asia and the Gulf region, where large Indian communities live and work.

The Factors Behind UPI's Rise

Several developments came together to make this transformation possible:

Government support for digital payments after 2016.

Affordable mobile internet that brought hundreds of millions online.

UPI's interoperable design, allowing any participating bank app to work seamlessly with another.

A user experience that is often faster and simpler than handling cash.

Most importantly, digital payments solved a real problem for both consumers and businesses.

A Habit That Is Becoming Permanent

The record set in May 2026 demonstrates that India's digital payments revolution is still gaining momentum.

Every month, new users adopt UPI. More merchants begin accepting digital payments. More transactions move away from cash.

What started as a technological innovation has evolved into a daily habit for hundreds of millions of Indians.

And with every scan of a QR code, the country moves one step closer to a future where paying with a phone is not the alternative-it is simply the default.

Tags

Work With Us

Need help identifying the right subsidy, preparing documentation, or maximizing claim value? Our team can guide you end to end.