Most Small Businesses Raising Money Today Aren't Expanding-They're Fighting to Stay Afloat

Most Small Businesses Raising Money Today Aren't Expanding-They're Fighting to Stay Afloat

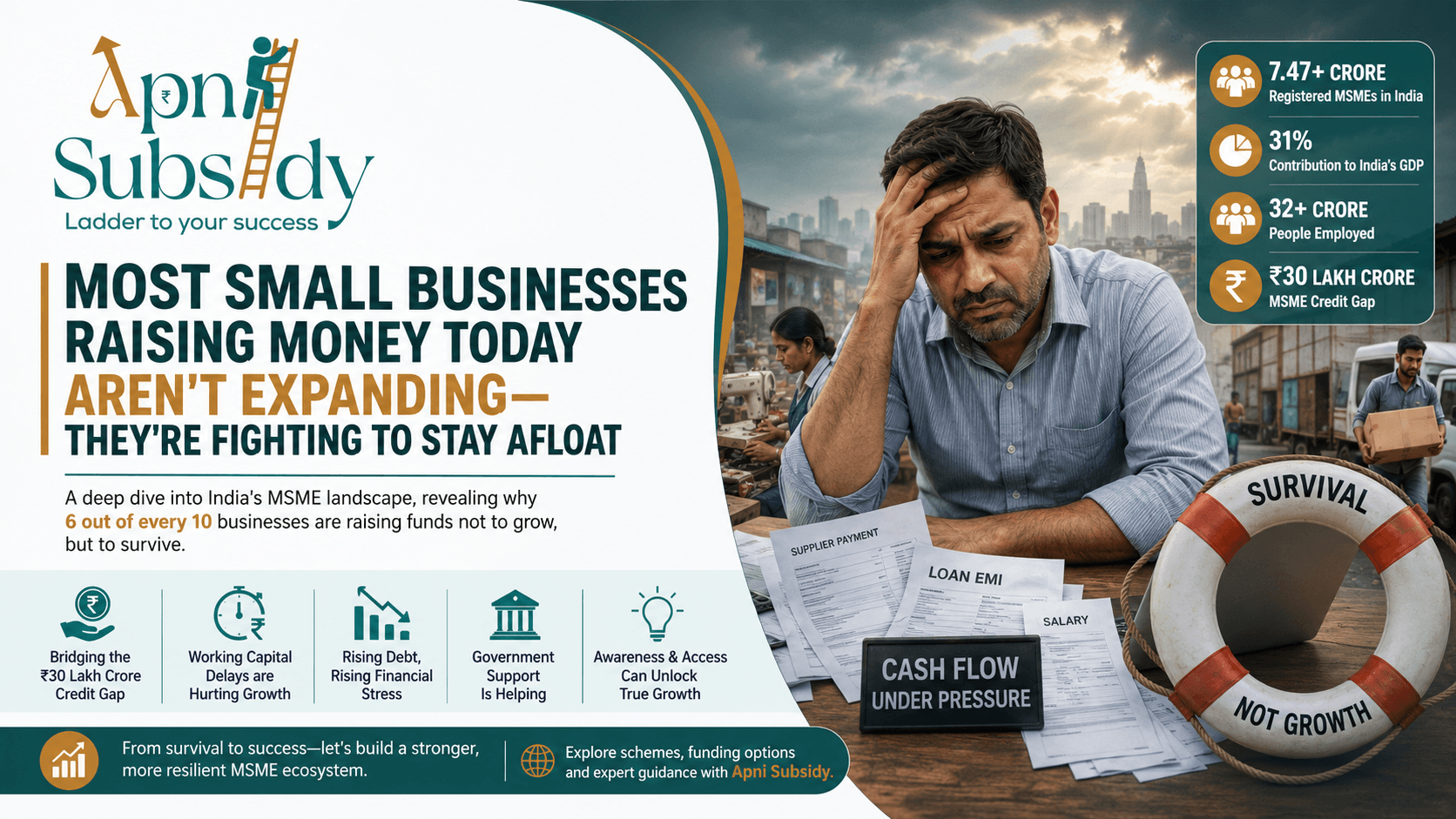

India's Micro, Small and Medium Enterprises (MSMEs) have long been celebrated as the backbone of the country's economy. They contribute nearly one-third of India's GDP, employ millions of people, and continue to drive entrepreneurship across cities, towns, and villages.

The numbers certainly tell an inspiring story. India now has more than 7.47 crore registered MSMEs, contributing around 31% of the nation's GDP while providing employment to over 32 crore people. Government initiatives have expanded access to formal registration, introduced credit guarantee schemes, simplified compliance, and encouraged digital adoption. On paper, the sector appears stronger than ever.

Yet beneath these impressive statistics lies a much more concerning reality.

Recent findings suggest that many small businesses are no longer borrowing money to grow-they are borrowing simply to survive.

A Concerning Shift in Why Businesses Need Capital

A June 2026 analysis by SMERGERS, a Bengaluru-based platform connecting businesses with investors and lenders, revealed a striking trend.

Out of the active fundraising mandates studied, six out of every ten MSMEs seeking investment or loans were not raising funds for expansion. Instead, they needed capital to:

Manage daily cash flow

Repay existing debts

Meet working capital requirements

Continue normal business operations

Very few were seeking funds to purchase new machinery, expand production, hire employees, or enter new markets.

That difference is more significant than it may first appear.

Businesses normally borrow because they see opportunities for growth. They invest today with the expectation of earning more tomorrow.

But when businesses borrow simply to pay existing bills, salaries, or suppliers, they are taking on additional financial risk just to keep operating. Survival funding rarely creates future growth-it merely postpones immediate financial pressure.

Why This Finding Matters

The businesses analysed by SMERGERS are not random local shops.

These are enterprises that have already prepared financial records, formally approached investors, and actively sought structured funding.

If businesses with enough organization to reach investment platforms are experiencing this level of financial stress, the challenges facing countless smaller and informal enterprises are likely even greater.

The report therefore offers an important snapshot of the wider condition of India's MSME ecosystem.

India's Persistent Credit Gap

One of the biggest reasons behind this situation is the country's long-standing MSME credit gap.

According to estimates from SIDBI and CRISIL, Indian MSMEs face a financing gap of nearly ₹30 lakh crore.

Simply put, the amount of credit that businesses actually require is far greater than what the formal banking system currently provides.

As a result, many enterprises experience one of two outcomes:

Their financing needs remain unmet.

They turn to informal lenders charging significantly higher interest rates.

Neither option supports sustainable business growth.

The Working Capital Challenge

Even profitable businesses can struggle because of cash flow timing.

Most MSMEs must pay suppliers within 45 days, as required under the MSMED Act. However, payments from customers—particularly large corporations or government departments-often arrive much later.

Delays of 60, 90, or even 120 days are not uncommon.

This creates a dangerous gap between money going out and money coming in.

During that period, businesses still have to pay salaries, rent, electricity bills, raw material costs, taxes, and other operating expenses.

Without sufficient working capital, even financially healthy businesses can quickly face liquidity problems.

A Growing Market Around Financial Distress

The SMERGERS analysis also highlighted another emerging trend.

Investor interest is increasing in businesses focused on debt resolution and recovery services.

While such services play an important role in financial markets, growing demand for them also reflects rising stress within the MSME sector.

When more businesses require restructuring or debt recovery support, it signals that financial pressure is spreading beyond isolated cases.

Government Support Has Made a Difference

Despite these challenges, it would be inaccurate to suggest that government efforts have not helped.

Over the past few years, several initiatives have strengthened the MSME ecosystem, including:

Credit Guarantee Fund Trust for Micro and Small Enterprises (CGTMSE)

Trade Receivables Discounting System (TReDS)

Pradhan Mantri Mudra Yojana

Export Promotion Mission

Self-Reliant India Fund

Udyam registration has expanded dramatically-from approximately 1.6 crore registered enterprises a few years ago to over 8.8 crore registrations today.

Similarly, the Self-Reliant India Fund has helped mobilize nearly ₹58,000 crore in equity support for eligible businesses.

These are meaningful achievements that continue to improve access to formal finance and business support.

Why Are Businesses Still Struggling?

If support schemes exist, why are so many businesses still raising money simply to stay operational?

There is no single answer.

Many entrepreneurs remain unaware of the schemes available to them.

Others find application procedures difficult to understand without professional guidance.

Structural issues such as delayed payments and limited access to affordable credit cannot be solved overnight.

Additionally, many of the businesses most in need operate in rural districts, informal sectors, or industries that traditional lenders find difficult to evaluate through standard credit models.

As a result, the gap between policy announcements and real-world benefits often remains significant.

A Story of Progress-and Pressure

India's MSME sector cannot be described as either a complete success or a complete failure.

Both realities exist simultaneously.

At the national level, the sector continues to grow, create employment, and contribute significantly to the economy.

At the business level, however, many entrepreneurs continue to face severe cash flow pressures, financing constraints, and delayed payments that threaten long-term sustainability.

Recognizing both sides of the story is essential for understanding the true state of India's small business landscape.

Looking Ahead

For small business owners, the recent findings carry an important message: if your business is currently raising funds primarily to manage cash flow, you are not alone. Thousands of enterprises across the country are facing similar challenges.

Seeking formal funding instead of relying on high-interest informal borrowing is still a positive step toward long-term financial stability.

For policymakers, lenders, and industry stakeholders, the findings highlight an equally important lesson.

Creating schemes is only the beginning. Ensuring that entrepreneurs can easily access them, understand them, and benefit from them is what will ultimately determine their success.

India's MSME sector has enormous potential. Unlocking that potential will require not only continued policy support but also faster access to credit, timely payments, greater awareness, and practical implementation that reaches businesses where they operate.

Only then can more entrepreneurs begin raising capital not simply to survive-but to grow.

Tags

Work With Us

Need help identifying the right subsidy, preparing documentation, or maximizing claim value? Our team can guide you end to end.

Get in Touch