When Paying Across the Border Becomes as Easy as Splitting a Bill

When Paying Across the Border Becomes as Easy as Splitting a Bill

India's UPI Expansion Is Quietly Transforming Cross-Border Payments

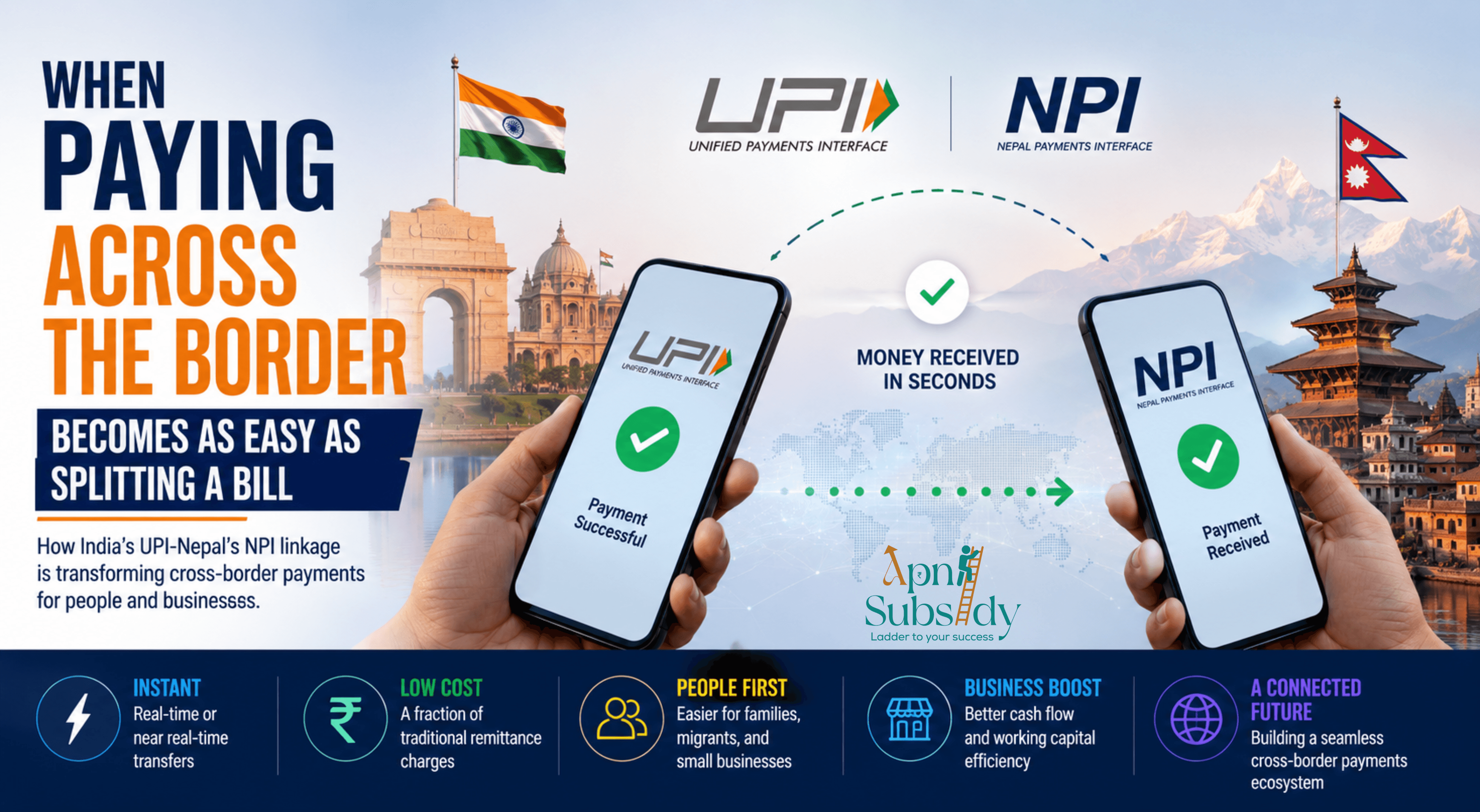

On June 6, a delivery rider in Kathmandu received money from his brother working in Delhi. It arrived in seconds—without a remittance agent, high transfer fees, or days of waiting. The transaction was processed through India's Unified Payments Interface (UPI), linked with Nepal's National Payments Interface (NPI), enabling near real-time cross-border transfers at a fraction of traditional costs.

While this may seem like a simple convenience, the India–Nepal payment corridor signals something much bigger. India is increasingly turning its domestic digital payments infrastructure into an exportable platform that could reshape how businesses, migrant workers, families, and traders move money across borders.

UPI's Scale Is Creating Global Opportunities

UPI has become the backbone of India's digital economy. In March 2026 alone, it processed 22.64 billion transactions worth nearly ₹29.53 lakh crore, with more than 500 million users relying on the platform.

Now, NPCI International—the overseas arm of the National Payments Corporation of India—is expanding that success globally through partnerships with foreign payment networks and financial institutions.

Why the India–Nepal Corridor Matters

The linkage does far more than help tourists make payments abroad. It creates a faster and more integrated payment experience between two neighboring economies with strong commercial and human ties.

For migrant workers, families, and businesses operating across the border, transfers that once depended on cash, remittance operators, or slow bank transfers can now move almost instantly. Faster settlement improves cash flow, reduces costs, and provides greater certainty for both individuals and businesses.

Immediate Benefits for MSMEs and Traders

The impact is especially significant for small businesses.

India and Nepal share an active trading relationship, with thousands of traders and small enterprises conducting cross-border business every day. Many operate with limited working capital, making payment delays costly.

Faster settlement allows money to circulate more efficiently, helping businesses improve inventory management, purchasing cycles, and day-to-day operations.

UPI's Growing International Reach

Nepal is part of a broader international expansion strategy.

UPI is already operational in various forms across countries including the UAE, Singapore, Bhutan, Mauritius, France, and Sri Lanka. While early partnerships focused on merchant payments for travelers, the emphasis is increasingly shifting toward remittances and deeper payment integration.

As additional partnerships emerge, Indian payment infrastructure could become accessible across a much larger global network.

What It Means for Exporters

For MSMEs and exporters, the long-term opportunity extends beyond convenience.

International payments have traditionally involved intermediary bank charges, foreign exchange costs, and settlement delays. As digital payment corridors mature, some of these frictions could decline significantly.

Lower costs and faster settlement would be particularly valuable for smaller exporters, where transaction fees often consume a larger share of revenue.

Challenges Remain

Despite the momentum, cross-border payments must navigate different legal and regulatory frameworks.

Issues such as data localization, anti-money laundering compliance, foreign exchange regulations, privacy requirements, and consumer protection will become increasingly important as transaction volumes grow.

However, the successful launch of new payment corridors suggests these challenges can be addressed through cooperation between governments, regulators, and payment operators.

A New Foundation for Cross-Border Commerce

For businesses in fintech, remittances, logistics, export services, and international trade, UPI's global expansion deserves close attention.

It is no longer just a domestic payment system. It is becoming a foundational layer for digital commerce, enabling money to move faster between people, businesses, and markets.

The India–Nepal corridor may seem modest today, but it offers a glimpse of a future where international payments become as seamless as splitting a bill with a friend—and for businesses operating across borders, that shift could be transformational.

Tags

Work With Us

Need help identifying the right subsidy, preparing documentation, or maximizing claim value? Our team can guide you end to end.

Get in Touch