Why That Rate Cut You Were Waiting For Isn't Coming

Why That Rate Cut You Were Waiting For Isn't Coming

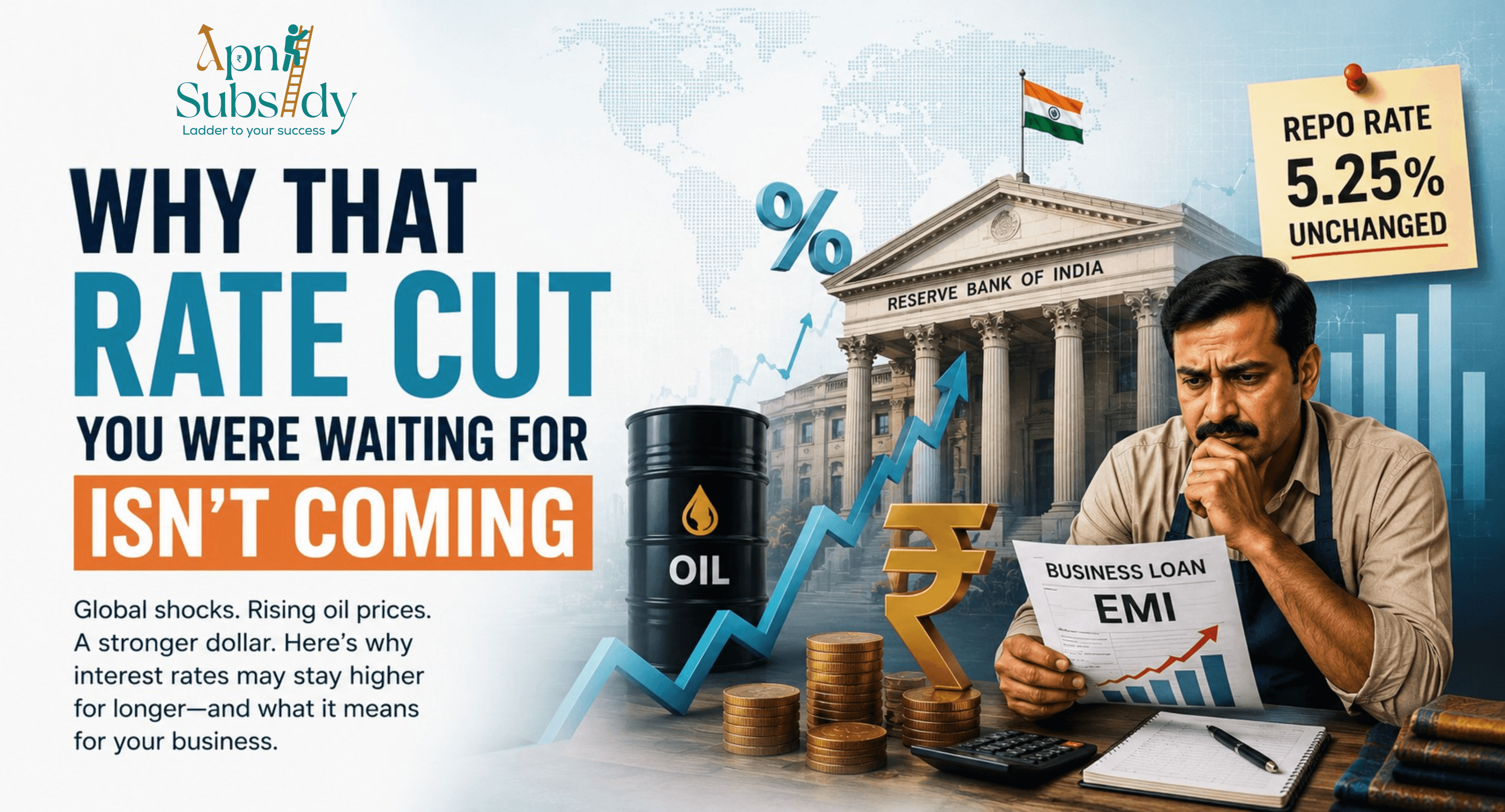

The Loan EMI Everyone Was Hoping Would Fall

A shop owner in a small town of India has been checking the news every few weeks for one simple reason: he's waiting for his business loan EMI to come down.

For months, that expectation seemed reasonable. Inflation was easing, economists were discussing rate cuts, and many businesses assumed borrowing costs would gradually decline.

Instead, the Reserve Bank of India (RBI) has chosen to keep the repo rate steady at 5.25 percent. More surprisingly, several central banks around the world that were expected to begin cutting rates have either delayed those plans or started raising rates again.

So why has the story changed so suddenly?

A Look Back: The Era of Cheap Money

To understand today's situation, it's worth going back to the 2008 global financial crisis.

When financial markets collapsed, central banks around the world—including the US Federal Reserve—slashed interest rates to near zero in an effort to support economic growth. Borrowing became exceptionally cheap, encouraging businesses and consumers to spend and invest.

That low-rate environment lasted for more than a decade.

Then came the COVID-19 pandemic.

Governments injected massive amounts of money into their economies to prevent collapse. Once lockdowns ended and demand returned, consumers suddenly had cash to spend while supply chains struggled to keep up. Prices surged across the world.

The war in Ukraine only made matters worse by disrupting food and energy supplies.

Central banks responded in the only way they could: by aggressively increasing interest rates to cool demand and fight inflation.

By the end of 2023, the US Federal Reserve had pushed rates to their highest level in more than twenty years before gradually easing them back toward the 3.5–3.75 percent range by late 2025.

India's Interest Rate Journey Was Different

India followed a different path.

When the 2008 crisis hit, the RBI cut the repo rate from around 9 percent to 4.75 percent within months to protect growth.

However, unlike many developed economies, India didn't enjoy years of ultra-low borrowing costs. Inflation returned relatively quickly, forcing the RBI to raise rates again, reaching around 8.5 percent by 2011.

The pandemic triggered another round of cuts, followed by another cycle of increases as inflation resurfaced.

By the end of 2025, the repo rate settled at 5.25 percent, a level many expected would soon begin moving lower.

That assumption is now being challenged.

The Global Picture Has Changed Again

Recent developments outside India are making central banks far more cautious.

The European Central Bank has raised its benchmark rate for the first time in three years. Countries including Indonesia, the Philippines, and Sri Lanka have also tightened monetary policy.

Attention has now shifted to the US Federal Reserve, where discussions have moved from "When will rates be cut?" to "Could rates rise again?"

The biggest reason is energy.

Growing tensions in West Asia have disrupted shipping through the Strait of Hormuz, one of the world's most important routes for crude oil and natural gas exports.

When that corridor faces disruptions, oil prices often climb rapidly. Higher fuel costs increase transportation expenses, manufacturing costs, and electricity prices, eventually feeding inflation across almost every sector of the economy.

At the same time, the US labour market remains unexpectedly strong, with robust job creation keeping consumer spending elevated and inflationary pressures alive.

Why This Matters for India

India may be geographically distant from these events, but it cannot ignore their economic consequences.

Domestic inflation remains within the RBI's target range, yet several risks remain.

Higher global oil prices raise transportation and production costs throughout the economy. A weaker monsoon could simultaneously push food prices higher.

The RBI's latest projections already estimate inflation at around 5.1 percent for the coming financial year—comfortably below crisis levels but still higher than policymakers would prefer.

The rupee has also weakened by roughly 4 percent against the US dollar since late February.

That combination leaves the RBI in a delicate position.

If the US Federal Reserve raises rates again, global investors may shift money toward dollar-denominated assets offering better returns. Capital outflows from India would place further pressure on the rupee, making imports more expensive and adding another layer of inflation.

In such an environment, maintaining higher interest rates becomes a defensive strategy rather than an aggressive one.

What Small Businesses Should Expect

For entrepreneurs waiting for cheaper loans, the outlook has become less encouraging.

Anyone planning to borrow for machinery purchases, inventory expansion, or additional working capital should not assume that today's interest rates are temporary highs.

They may instead represent the baseline for the foreseeable future.

Businesses that depend on imported equipment or raw materials face another challenge. A weaker rupee increases the cost of goods priced in US dollars, raising investment costs even if domestic demand remains healthy.

The Bottom Line

The key takeaway isn't that India will definitely raise interest rates tomorrow.

Rather, it's that the widespread assumption that borrowing costs would only move downward has quietly stopped being reliable.

Global energy markets, geopolitical tensions, exchange rates, and decisions made by central banks thousands of kilometres away are increasingly shaping the cost of borrowing for Indian businesses.

For now, companies planning their finances may be better served by preparing for interest rates to stay elevated rather than waiting for relief that may not arrive anytime soon.

Tags

Work With Us

Need help identifying the right subsidy, preparing documentation, or maximizing claim value? Our team can guide you end to end.

Get in Touch