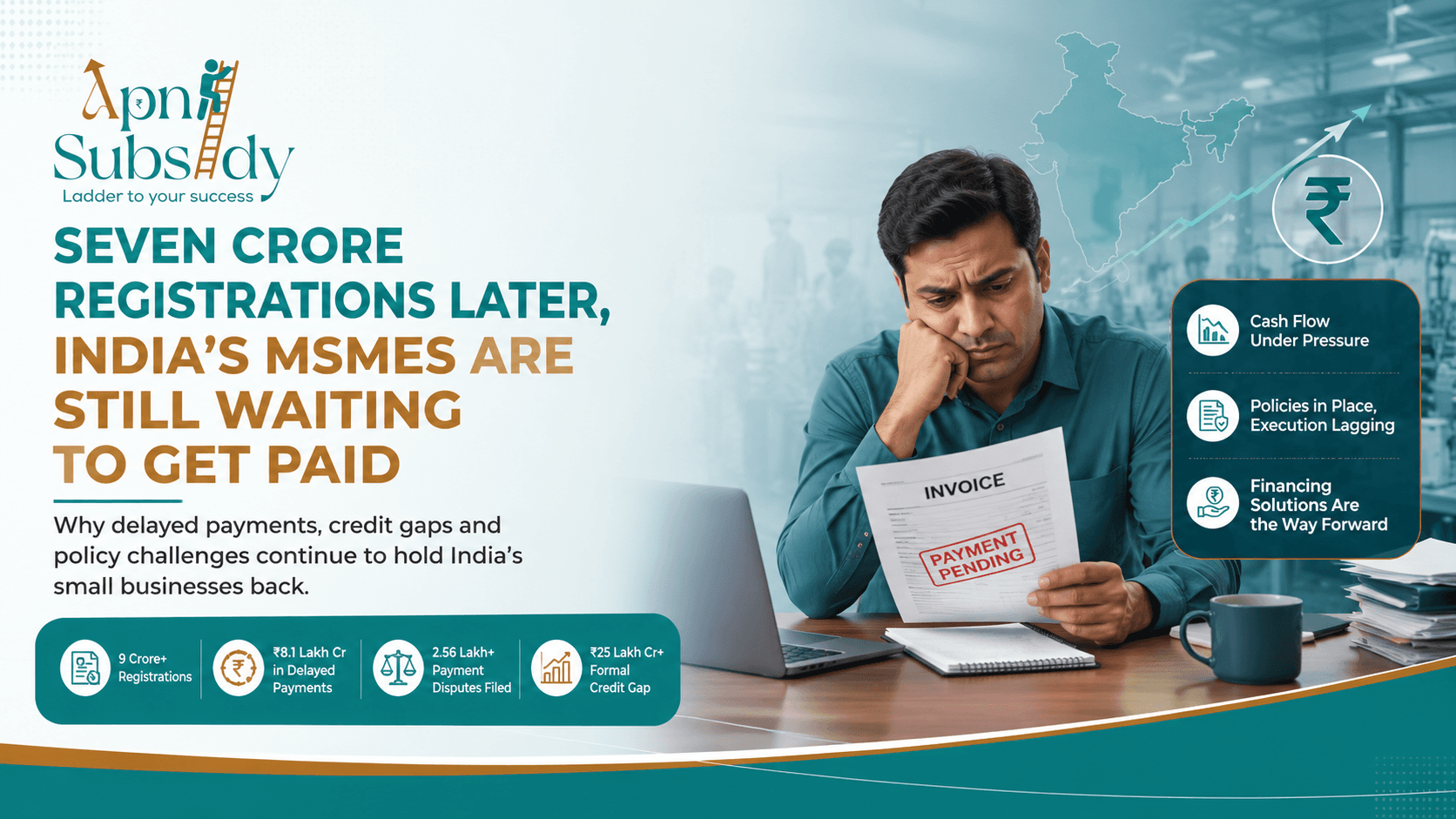

Seven Crore Registrations Later, India's MSMEs Are Still Waiting to Get Paid

Seven Crore Registrations Later, India's MSMEs Are Still Waiting to Get Paid

For years, India's MSME story has been one of remarkable growth.

The sector now contributes nearly one-third of the country's GDP, accounts for almost half of India's merchandise exports, and supports close to 39.5 crore jobs. With the rapid expansion of the Udyam Registration system and the Udyam Assist Platform, nearly nine crore enterprises have entered the formal economy, giving policymakers an unprecedented understanding of India's small-business landscape.

On paper, this looks like one of the biggest success stories in India's economic transformation.

But behind these impressive numbers lies a much less encouraging reality.

For thousands of small businesses across the country, the biggest challenge isn't starting a business, registering under Udyam, or even finding customers.

It's getting paid.

India's MSMEs Are Becoming More Visible-Not Necessarily More Secure

During World MSME Day in June, the government announced several digital initiatives, upgraded online portals, and highlighted the rapid formalisation of India's small-business ecosystem.

At the same time, reports presented before Parliament and reviews by the Ministry of MSME revealed an uncomfortable truth.

While registrations have grown at record speed, financial security hasn't.

Businesses are entering the formal system faster than ever before, but many continue to struggle with delayed payments, working capital shortages, and inconsistent cash flow.

In other words, formalisation has accelerated-but financial stability hasn't kept up.

When Almost Everyone Is a Micro Enterprise

Another challenge has emerged from the revised MSME classification introduced in 2025.

The government significantly increased both investment and turnover limits, allowing businesses to expand without immediately losing the benefits associated with MSME status.

The objective was sensible.

Growing businesses shouldn't be penalised simply because they became slightly larger.

However, the new classification has created an unintended consequence.

Today, an overwhelming majority of registered businesses fall under the "micro enterprise" category.

That means a small home-based manufacturer operating with limited resources can now fall into the same category as a business that has invested crores in machinery and generates substantially higher turnover.

Although both technically qualify as micro enterprises, their financial needs, operational challenges, and growth potential are entirely different.

As more businesses share the same classification, designing targeted government support becomes increasingly difficult.

The Biggest Problem Isn't Orders. It's Payments.

Delayed payments continue to be one of the most serious threats facing India's MSME sector.

According to the Economic Survey, unpaid dues owed to MSMEs have now reached approximately ₹8.1 lakh crore.

The numbers become even more concerning when looking at dispute resolution.

Since its launch, the MSME Samadhaan Portal has received over 2.56 lakh payment-related complaints, involving claims exceeding ₹55,000 crore.

Yet only a little over one-fifth of these cases have been resolved through the designated Facilitation Councils.

To improve recovery, the government also introduced an Online Dispute Resolution (ODR) system intended to make settlements faster and more technology-driven.

However, according to the Parliamentary Standing Committee, the platform managed to dispose of only 17 cases during its initial months.

The contrast is difficult to ignore.

India has built sophisticated digital platforms for registrations, compliance, and dispute filing.

But when businesses actually need their money, the recovery process remains painfully slow.

When Good Policy Creates Unexpected Problems

One of the government's strongest attempts to improve payment discipline came through Section 43B(h) of the Income Tax Act.

The rule requires buyers to pay registered micro and small enterprises within prescribed timelines if they wish to claim tax deductions.

The objective was straightforward.

Encourage faster payments by making delayed payments financially disadvantageous for buyers.

But the market didn't always respond the way policymakers expected.

Several industries have reported that instead of changing their payment practices, some larger buyers simply became reluctant to purchase from registered MSMEs altogether.

Rather than improving payment behaviour, the regulation has, in certain cases, influenced purchasing behaviour.

It's a reminder that policy outcomes often depend as much on market incentives as on legal provisions.

The Government Is Now Focusing on Financing Infrastructure

Recognising that compliance alone cannot solve the payment problem, recent policy efforts have shifted toward improving financing mechanisms.

The Union Budget proposed a ₹10,000 crore SME Growth Fund, expanded support for the Self-Reliant India Fund, and strengthened the Trade Receivables Discounting System (TReDS).

These platforms allow MSMEs to discount their invoices and receive payments earlier instead of waiting months for buyers to clear outstanding dues.

Collectively, TReDS platforms have already facilitated invoice financing worth more than ₹7 lakh crore.

The government is also encouraging greater participation from public sector enterprises, hoping invoice discounting becomes a standard business practice rather than an exception.

If implemented effectively, this could significantly improve liquidity for small businesses.

India's Credit Gap Is Much Bigger Than Delayed Payments

Late payments are only one part of a much larger financial challenge.

Industry estimates suggest India's MSME sector faces a formal credit gap exceeding ₹25 lakh crore.

A significant number of businesses still rely on informal borrowing because they lack access to institutional finance.

This creates a major opportunity for the private sector.

Fintech lenders, invoice-financing platforms, embedded finance providers, and alternative credit assessment models are increasingly stepping in to evaluate businesses based on actual cash flows instead of traditional collateral requirements.

For many MSMEs, these innovations could prove just as important as government support schemes.

What Entrepreneurs Should Learn From This

For business owners, registration remains valuable.

It provides access to government procurement opportunities, priority sector lending, subsidy schemes, and various MSME support programs.

But registration alone doesn't guarantee financial health.

Strong cash flow remains the foundation of every successful business.

Choosing customers with reliable payment histories, actively using receivables financing platforms like TReDS, maintaining tighter financial discipline, and monitoring working capital can often make a greater difference than simply obtaining an MSME certificate.

Formal recognition is important.

Financial resilience is even more important.

The Road Ahead

India deserves recognition for bringing millions of informal businesses into the formal economy.

Few countries have formalised enterprises at this scale within such a short period.

That achievement will influence policymaking, taxation, lending, and business support for years to come.

But the next phase of India's MSME journey cannot be measured only by the number of registrations.

It must be measured by whether those businesses become financially stronger.

Because for entrepreneurs, success isn't defined by a registration certificate.

It's defined by something much simpler.

Whether the payment arrives when the invoice says it should.

Tags

Work With Us

Need help identifying the right subsidy, preparing documentation, or maximizing claim value? Our team can guide you end to end.

Get in Touch