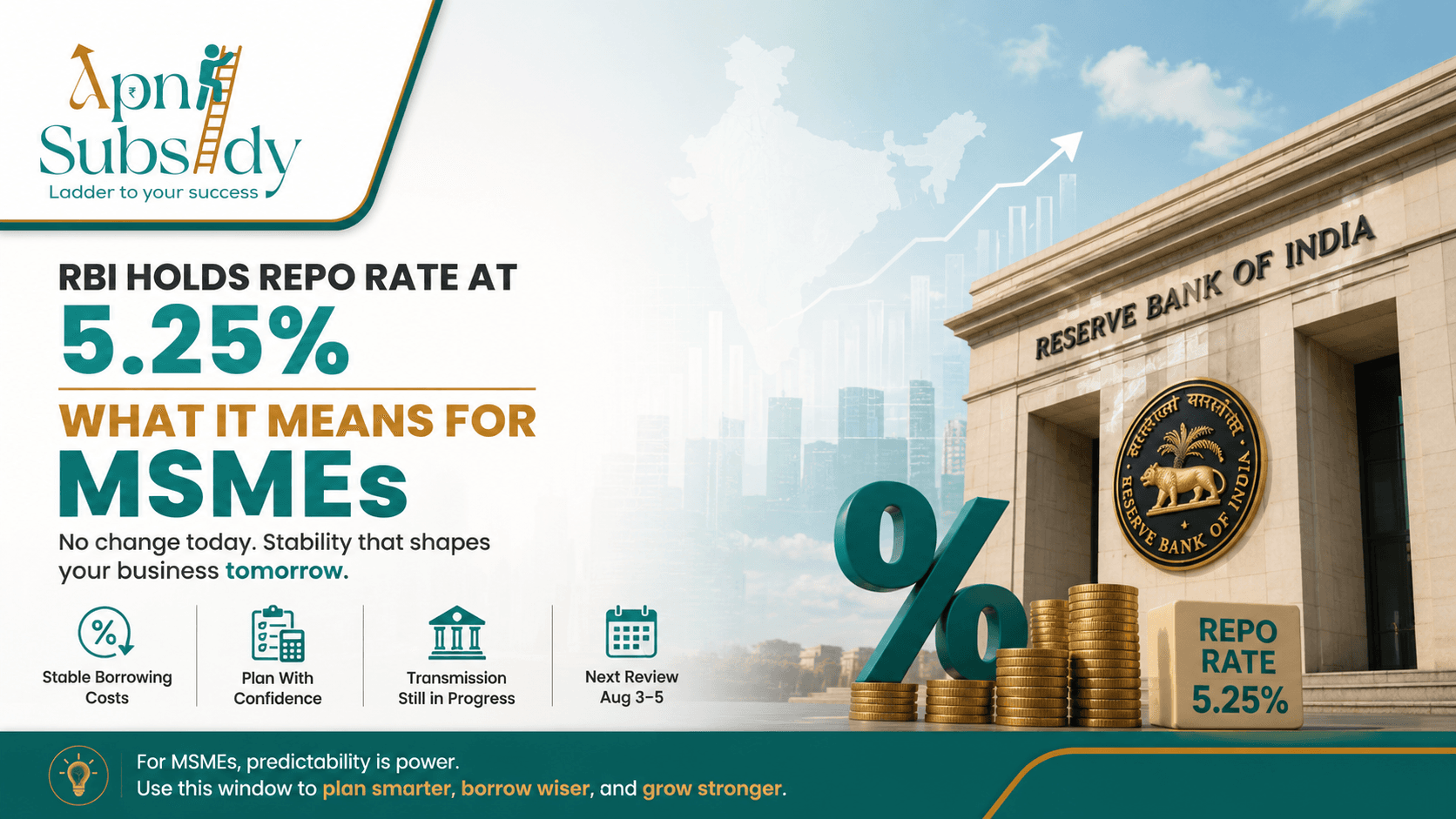

The RBI Didn't Change Interest Rates. Here's Why That Still Matters for Every MSME.

The RBI Didn't Change Interest Rates. Here's Why That Still Matters for Every MSME.

When the Reserve Bank of India's Monetary Policy Committee met in June, the headline looked almost uneventful.

The repo rate stayed exactly where it was-5.25 percent.

No surprise rate cut. No unexpected hike. No dramatic market reaction.

For many business owners juggling GST filings, vendor payments, and customer orders, a "no change" announcement is easy to ignore.

But for India's nearly six crore MSMEs, whose day-to-day operations depend heavily on bank financing, a decision to leave interest rates unchanged is far from meaningless. In fact, stability itself can shape borrowing decisions, cash flow planning, and business expansion over the coming months.

Why the Repo Rate Matters

The repo rate is the interest rate at which the RBI lends money to commercial banks. It acts as the benchmark that influences the interest rates banks charge businesses and consumers.

Today, most new business loans are linked to the External Benchmark Lending Rate (EBLR), meaning changes in the repo rate usually flow through to borrowers relatively quickly.

When the RBI cuts rates, loan EMIs typically fall.

When it raises rates, borrowing becomes more expensive.

When it keeps rates unchanged, businesses continue borrowing at the existing cost.

For MSMEs, that means one thing: the cost of borrowing remains predictable.

Stability Can Be an Advantage

The next RBI policy review is scheduled between August 3 and August 5.

Until then, entrepreneurs planning to purchase machinery, build inventory, expand operations, or simply bridge temporary working capital gaps know exactly what borrowing will cost.

That certainty may not generate headlines, but it makes financial planning significantly easier.

For businesses operating with tight margins and limited cash reserves, knowing that interest costs won't suddenly change can be just as valuable as a rate cut.

Why the RBI Chose to Wait

The central bank is trying to balance two competing priorities.

On one side is inflation, which has remained comfortably within the RBI's target range, supported by softer crude oil prices and healthy agricultural output.

On the other side is economic growth, which remains steady but not exceptionally strong.

Cutting interest rates further could stimulate borrowing and investment-but it could also reignite inflationary pressures.

Instead, the RBI has chosen to wait and observe how previous rate cuts made through late 2024 and early 2025 continue to influence the economy before making another move.

Why MSMEs Feel the Impact More Than Large Companies

Large corporations have multiple financing options.

They can raise capital through bond markets, negotiate customized credit facilities, or access international financing.

MSMEs don't usually have those alternatives.

Most depend almost entirely on commercial bank loans.

And that's where another challenge appears.

Historically, banks have been slower to pass repo rate reductions on business loans than they have been for home loans or personal loans.

That means an RBI rate cut announced months ago may still not have fully translated into lower borrowing costs for many small businesses.

In other words, some MSMEs may still be waiting to receive the full benefit of previous monetary easing.

It's Not Just About Loans

Interest rate decisions also affect businesses that maintain fixed deposits or temporarily park surplus cash.

With the repo rate unchanged:

Fixed deposit returns are likely to remain broadly stable.

Deposit rates aren't expected to improve immediately.

Businesses earning interest on idle funds won't see significant changes before the next policy review.

For MSME owners managing both borrowing and savings, this creates a relatively stable financial environment on both sides of the balance sheet.

What MSMEs Should Do Right Now

Rather than focusing on what the RBI didn't do, business owners should use this period of stability wisely.

If you already have a floating-rate business loan, verify whether your bank has fully passed on the benefits of previous repo rate cuts. Many banks don't automatically revise lending rates, and transmission delays remain common.

If you're considering taking a new loan, today's stable interest-rate environment provides a reliable basis for budgeting and repayment planning over the next few weeks.

At the same time, keep a close eye on the RBI's August policy meeting. The central bank has deliberately left itself room to either reduce or increase rates depending on how inflation and economic growth evolve during the coming months.

The Bottom Line

A monetary policy announcement that delivers "no change" rarely captures public attention.

Yet for India's MSME sector, where every percentage point on a working capital loan directly affects profitability, the RBI's decision to hold rates steady is more than just a pause.

It offers predictability.

It allows businesses to plan with greater confidence.

And it gives entrepreneurs a valuable window to review financing decisions before the RBI makes its next move.

Sometimes, in business, certainty can be just as valuable as change.

Tags

Work With Us

Need help identifying the right subsidy, preparing documentation, or maximizing claim value? Our team can guide you end to end.

Get in Touch