When India Finally Forced the Cheque to Clear

When India Finally Forced the Cheque to Clear

For decades, India's small businesses have faced a familiar problem. They complete the work, deliver the goods, raise the invoice—and then wait.

Sometimes for 60 days. Sometimes 90. Often even longer.

The buyers are usually large corporations or government enterprises with enough financial strength to delay payments without much consequence. Meanwhile, the small supplier struggles to manage cash flow, often taking expensive loans just to keep operations running.

In many ways, MSMEs have been unknowingly financing the working capital needs of businesses much larger than themselves.

The Union Budget 2026-27 may have taken a significant step toward changing that.

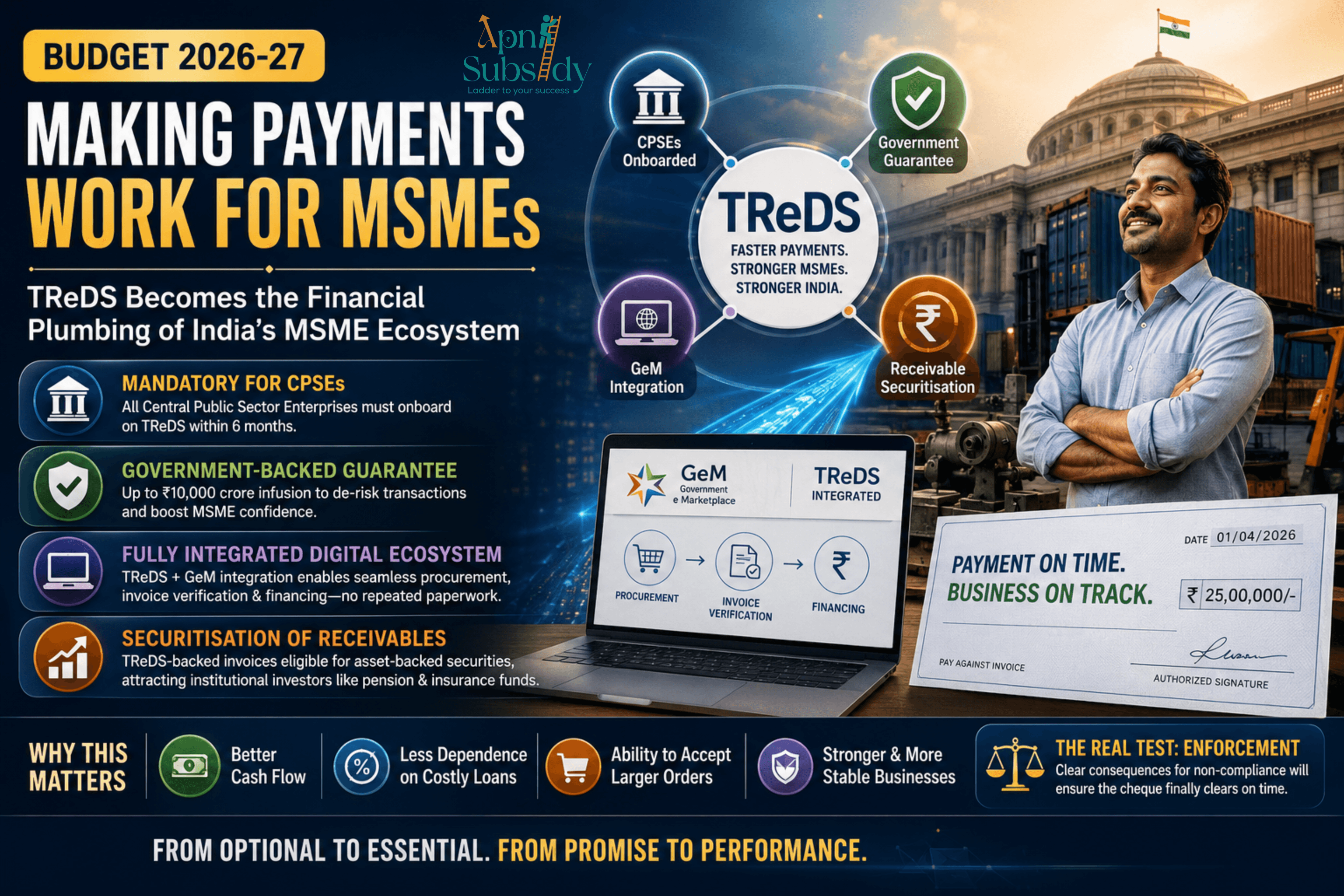

The Big Move: Mandatory TReDS for CPSE Purchases

The government's biggest MSME liquidity reform this year is the mandatory use of the Trade Receivables Discounting System (TReDS) for all purchases made by Central Public Sector Enterprises (CPSEs) from MSME suppliers.

While TReDS has existed for years, its adoption remained limited because participation was largely voluntary. The government had previously encouraged companies to register and even reduced the mandatory registration threshold to companies with turnover above ₹250 crore.

However, encouragement only goes so far.

This year's Budget moves beyond encouragement and makes participation compulsory for CPSE procurement, marking a major shift in policy.

What Exactly Is TReDS?

TReDS is a digital platform introduced by the RBI in 2017.

The system allows MSMEs to upload approved invoices and receive financing from banks and financial institutions through a competitive bidding process.

Instead of waiting months for payment:

The MSME gets cash almost immediately.

The financier earns a discount fee.

The buyer pays on the original due date.

In theory, it solves one of the biggest challenges faced by small businesses—delayed payments.

The challenge has never been the platform itself. The challenge has been adoption.

Although TReDS processed around ₹3.6 lakh crore worth of transactions last year, estimates suggest total delayed MSME receivables in India range between ₹8 lakh crore and ₹10 lakh crore annually.

The platform worked.

Too few businesses used it.

The Budget's Four-Part Strategy

The government has now introduced a broader package designed to make TReDS a core part of India's financial infrastructure.

1. Mandatory CPSE Participation

Large public-sector buyers must now route MSME payments through TReDS, bringing some of the country's most creditworthy buyers onto the platform.

2. CGTMSE Guarantee Support

The Credit Guarantee Fund Trust for Micro and Small Enterprises (CGTMSE) will provide guarantee support for invoice discounting on TReDS.

This reduces risk for financiers and makes it easier for smaller MSMEs to access funding.

3. GeM-TReDS Integration

The Government e-Marketplace (GeM) will be integrated with TReDS.

This means procurement, invoice verification, and financing can happen through a connected digital ecosystem instead of separate systems with repeated paperwork.

4. Securitisation of Receivables

TReDS-backed receivables will be eligible for asset-backed securities.

If implemented successfully, this could attract institutional investors such as pension funds and insurance companies into MSME financing, significantly expanding the availability of working capital.

Why This Matters for MSMEs

India now has approximately 7.6 crore enterprises registered under Udyam.

Most of them struggle with working-capital shortages and delayed payments.

For these businesses, faster invoice settlement can mean:

Better cash flow

Reduced dependence on expensive loans

Greater ability to accept larger orders

Improved business stability

Industry experts believe this reform could transform TReDS from a niche fintech solution into a critical part of India's financial infrastructure.

In simple terms, it is moving from being an optional service to becoming part of how government procurement payments are processed.

RBI Is Also Strengthening the Framework

The RBI has been working alongside these reforms.

In April 2026, it released draft TReDS Directions aimed at streamlining and harmonising the rules governing the platform.

While this may sound like a technical update, it signals something important:

The regulator increasingly sees TReDS as permanent financial infrastructure rather than a pilot project or experimental initiative.

The Real Challenge: Enforcement

Despite the optimism, one important question remains.

Will the rules actually be enforced?

India has introduced delayed-payment penalties and complaint mechanisms before, but implementation has often been inconsistent.

The real test will come when a CPSE fails to comply with TReDS requirements.

If there are clear consequences for non-compliance, the reform could fundamentally improve payment discipline across public procurement.

If enforcement remains weak, many of the intended benefits could be diluted.

Final Thoughts

The Budget 2026-27 is attempting something larger than simply expanding a fintech platform.

It is trying to transform TReDS into the financial plumbing of India's MSME ecosystem.

The combination of mandatory CPSE participation, government-backed guarantees, GeM integration, and receivable securitisation creates a more complete framework than previous attempts to tackle delayed payments.

Whether it succeeds now depends less on policy design and more on execution.

For millions of India's small businesses, the question is no longer whether the system exists.

The question is whether the cheque will finally clear on time.

Tags

Work With Us

Need help identifying the right subsidy, preparing documentation, or maximizing claim value? Our team can guide you end to end.

Get in Touch